MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

FOR IMMEDIATE RELEASE New York Press Office: (212) 346-5500; media@iii.org

Florida Press Office: (813) 480-6446; lynnem@iii.org

TAMPA, Florida, May 6, 2015 — While the last major hurricanes to strike Florida date back to 2005, flooding is a more common occurrence. Indeed, just last year, historic rainfall in the western Florida Panhandle brought more than 20 inches of rainfall that inundated Pensacola in April 2014. It can rain hard on any given day in Florida—and for extended periods. For that reason, all Floridians should consider getting a flood insurance policy, according to the Insurance Information Institute (I.I.I.), even those who don’t live on the coastline.

“There’s a risk of flooding for people living inland because the water has to go somewhere, and that means rivers and streams can rise rapidly in the days following torrential rainfall,” said Lynne McChristian, Florida spokesperson for the I.I.I. “Powerful storms like hurricanes grab the headlines, but slow-moving tropical storms bringing huge amounts of rain can cause equally damaging inland floods.”

Standard homeowners insurance policies do not cover flood damage. A separate flood policy is required, which is available from the National Flood Insurance Program (NFIP) or through a few private insurance companies. The average flood insurance policy for a homeowner, which includes coverage for both contents and the structure itself, costs $700, according to the NFIP. Private excess flood insurance is also available if more coverage is needed than the maximum amount available from the NFIP.

Renters need flood insurance, too. Most renters living in low- to moderate-risk flood zones are eligible for preferred rates, with contents-only coverage ranging from $44 to $266 a year, depending on the flood zone and amount of coverage. Detailed information on the National Flood Insurance Program can be found at www.floodsmart.gov.

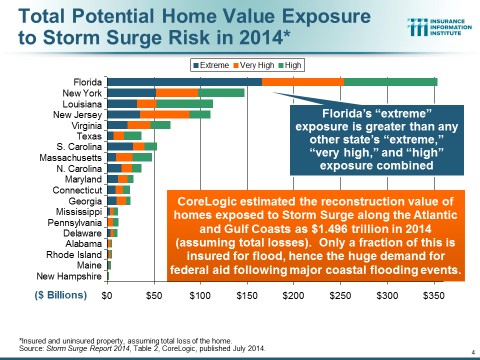

Recent flood insurance reforms are phasing in for areas at high risk for flooding, and flood maps are being updated to move some people into higher- or lower-risk zones. However, there are no “zero-risk zones.” It is important to recognize that Florida has more property at risk to storm surge than any other state. And storm surge does not threaten only coastal residents, as rising tidal waters can move inland. This makes Florida the U.S. state most at risk for flooding (see chart below). Florida may have more flood insurance policies in force than any other state, but the percentage is still small compared to the likelihood of flooding. The number of flood policies in Florida, as of February 2015, totaled more than 1.9 million; however there are over 7.3 million housing units.

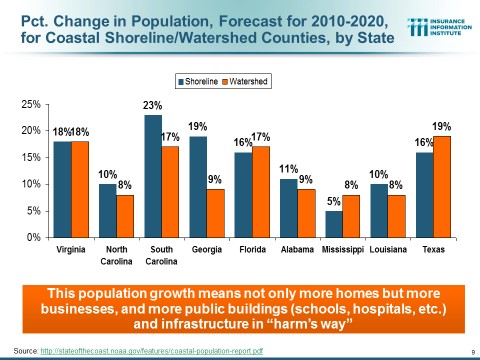

Florida’s risk for storm surge is also increasing with new construction and new residents flocking to coastal locales. NOAA’s “State of the Coast” report notes a 45 percent increase in people living in coastal watershed counties between 1970 and 2010, and the trend will continue (see chart below). By 2020, Florida is expected to see a 16 percent increase in people living near the shoreline.

The I.I.I. encourages Floridians to have a conversation with their insurance professional to make sure their coverage is up to date. Keep in mind that flood insurance policies through the NFIP have a 30-day waiting period before they go into effect, so do not wait for a severe weather warning to start looking into flood protection.

RELATED LINKS

Issues Update: Flood Insurance Facts and Statistics: The National Flood Insurance Program; Florida Hurricane Fact File

The I.I.I. has a full library of educational videos on its You Tube Channel. Information about I.I.I. mobile apps can be found here.

THE I.I.I. IS A NONPROFIT, COMMUNICATIONS ORGANIZATION SUPPORTED BY THE INSURANCE INDUSTRY.