The Florida House’s attempt to curtail recent legal system reforms met firm resistance from the state Senate this week, preserving the 2022 and 2023 legislation that stabilized the state’s property insurance market.

Aiming to reinstate one-way attorney fees in insurance litigation, the House added an amendment – originally part of a separate bill – to an unrelated Senate bill focused on creating legal protections for owners of former mining sites.

Filed by state Rep. Berny Jacques, the amendment would have restored Florida’s previous requirement for insurers to shoulder the insured’s legal costs, even if the insured’s jury award was only slightly higher than the settlement insurers offered. Current law stipulates that each side is responsible for their own fees.

Senate members refused to concur with the proposal and sent the bill back to the House, which can either remove Jacques’ amendment or let the entire bill die.

Insurers and policyholders benefit

Jacques’ amendment prompted instant criticism from industry leaders, notably Florida Insurance Commissioner Michael Yaworsky, who sent an email warning the governor’s legislative affairs director that it would dismantle “hard-won progress” achieved by the 2022-2023 reforms, according to a report by the South Florida Sun Sentinel.

That progress includes the introduction of 12 new insurers into Florida’s property sector after a multi-year exodus and a 23 percent decrease in lawsuit filings year over year, Yaworsky wrote.

Proponents of Jacques’ amendment argued it would return balance to the legal system, which had overcorrected to favor insurance companies at the expense of consumers.

Yet, in 2019, Florida accounted for just over 8 percent of U.S. homeowners insurance claims, but more than 76 percent of U.S. property claim lawsuits, pushing premium rates up to three times the national average. Post-reform, in 2024, 40 percent of all insurers in the state filed for rate decreases, with average home insurance premiums down 5.6 percent at the start of this year.

Reversing these reforms would reinvigorate fraudulent and unnecessary lawsuits, increasing insurer costs and, consequently, premium rates. Dulce Suarez-Resnick, an insurance agent based in Miami, told the Sun Sentinel that supporters predicted reforms wouldn’t be felt for three years.

“We are two years in, and I’ve already seen a lot of impact,” Suarez-Resnick said. “The Legislature needs to be patient. We have one more year to go.”

Reforms expected to remain intact

Though Florida’s 2025 legislative session was extended, the House has little time to push for further changes to the reforms. Even if the Senate somehow acquiesces and passes the amended bill, it is unlikely to survive – Gov. Ron DeSantis has vowed to veto any bill targeting tort reform and publicly condemned the House’s efforts to roll it back.

And Florida isn’t alone: Georgia successfully passed its own comprehensive tort reform package last month, after plaintiffs’ attorneys began transferring their marketing tactics to the neighboring state. State government moves like these are essential to eradicating legal system abuse and protecting all stakeholders from rising costs.

Established by Congress through the Disaster Recovery Reform Act of 2018, the BRIC program has allocated more than $5 billion for investment in mitigation projects to reduce economic losses from floods, wildfires, and other disasters for hundreds of communities. Ending BRIC will cancel all applications from 2020-2023 and rescind more than $185 million in grants intended for Louisiana, leaving the 34 submitted and accepted projects funded by those grants in limbo.

Whereas the FEMA press release described BRIC as “wasteful and ineffective,” Cassidy identified “not doing the program and then having to rescue communities when the inevitable flood occurs – that is waste, because we could have prevented that from happening in the first place.”

A 2024 study backed by the U.S. Chamber of Commerce supports this claim, which found that disaster mitigation investments save $13 in benefits for every dollar spent.

FEMA’s decision coincides with recovery efforts in Natchitoches, a small Louisiana city, after flash flooding inundated homes and downed power lines just weeks before. BRIC was set to fund improvements to the city’s backup generator system to pump out floodwater during severe weather.

Similarly, Lafourche Parish will lose $20 million to strengthen 16 miles of power lines, which Cassidy noted toppled “like dominos” during last year’s Hurricane Francine. Jefferson Parish residents displaced following Hurricane Ida in 2021 will lose the home elevation disaster grants they finally secured earlier this year.

“Louisiana was the third-largest recipient of BRIC’s most recent round of funding and is the largest recipient on a per capita basis,” Cassidy said. “Without BRIC, none of these projects would be possible.”

A national problem

Beyond Louisiana, Cassidy pointed to numerous states ravaged by severe storms so far this year, particularly inland communities where flooding is traditionally unexpected. At least 25 people died amid a severe weather outbreak across the southern and midwestern U.S. last month, underscoring a growing need for resiliency planning in non-coastal areas.

BRIC is one of many programs facing sudden termination under the Trump Administration. Twenty-two states and the District of Columbia have filed a lawsuit demanding the federal government unfreeze essential funding, including BRIC grants. Though the administration is reportedly complying with a federal judge’s order blocking the freeze, the states involved claim funding remains inaccessible.

Louisiana has not joined the lawsuit, but Cassidy emphasized the congressional appropriation of the program and requested the fulfillment of preexisting BRIC applications. He argued that “to do anything other than use that money to fund flood mitigation projects is to thwart the will of Congress.”

As President Trump weighs disbanding FEMA entirely – even as FEMA responds to record-breaking numbers of billion-dollar disasters – it is imperative to recognize the vast co-beneficiary benefits of disaster resilience, and develop our partnerships across these stakeholder groups.

The National Weather Service (NWS) – part of the National Oceanic and Atmospheric Administration (NOAA) – recently announced that it was reducing the number of weather balloons it launches across the country, citing staffing shortages at 11 NWS locations.

The launch cuts followed NOAA’s announcement of hundreds of layoffs or voluntary resignations across the agency, including at the NWS, related to efforts by President Donald Trump’s Department of Government Efficiency (DOGE). Former NOAA Administrator Rick Spinrad said in a press conference that about 650 NOAA employees were among those fired, and his former colleagues in the agency said they had been ordered to “identify another 1,029 positions” for termination.

Some of these suspensions – for example, in Omaha, Neb. – have been lifted. Two meteorologists are set to arrive from across the country to staff the Omaha office following lobbying from Rep. Mike Flood (R. – Neb).

However, the future of launches from the remaining 10 locations remains unclear.

What do weather ballons do?

Apart from occasionally being taken for extraterrestrial aircraft, weather balloons rarely attract public attention. Carrying a device called a “radiosonde”, they typically fly for a couple of hours – potentially reaching 100,000 feet – and are used for several purposes, from gathering data for weather prediction models and local forecasts to providing input for pollution and climate research.

“Weather balloon launches can be especially critical in severe storm situations,” said Dr. Phil Klotzbach, a researcher at Colorado State University and a Triple-I non-resident scholar. “They give us detailed information on temperature, pressure, and humidity that can help us determine potential impacts from tornadoes and hail.”

In addition, Klotzbach said, before U.S. hurricane landfalls, “NWS offices will often coordinate additional weather balloon launches to provide critical data to weather forecast models that improve predictions of the hurricane’s track.”

“While satellite technology continues to improve and provides invaluable information that has dramatically improved forecasting ability over the past several decades, weather balloons still serve a vital role in helping to predict weather events,” Klotzbach said.

Taken-for-granted resources highlighted

As with the Federal Emergency Management Agency’s recent termination of its Building Resilient Infrastructure and Communities (BRIC) grant and loan program, the sudden and substantial downsizing of NOAA’s data-gathering and forecasting resources underscores the extent to which government agencies that operate below the public’s radar screen help society and industry take steps to avoid costly losses related to weather- and climate-related events.

In the absence of reliable federal support, it’s more important than ever for families, communities, businesses, and other stakeholders to work together to mitigate risks and build resilience. The insurance industry is uniquely well positioned to support and advance these efforts.

New, alarming financial risks for homebuyers who are unaware of property flood histories has driven several states to implement new disclosure laws, helping protect consumers from unexpected costs after purchasing flood-prone homes, according to new research from Milliman.

Atmospheric conditions are intensifying flood risks across the U.S., with severe storms and rain events becoming more devastating and frequent. Despite this escalating threat, a significant regulatory gap has persisted: many states haven’t required home sellers to disclose previous flooding to potential buyers.

This omission creates a dangerous scenario where unsuspecting homebuyers invest their savings in properties with undisclosed flood histories.

As Joel Scata, senior attorney in the climate adaptation division at the Natural Resources Defense Council (NRDC), explains, “If a buyer doesn’t know the house is flood-prone, they don’t know they need to buy flood insurance. They don’t know they need to mitigate that risk, and that they could be in a really bad situation when the next flood happens.”

The issue became impossible to ignore in 2018 when Hurricane Florence inundated more than 74,000 buildings in North Carolina. At that time, sellers weren’t required to inform buyers about previous flooding, meaning hurricane-damaged homes could be cleaned up and sold without disclosure of this critical history. Since properties that have flooded once are likely to flood again, this lack of transparency created significant financial vulnerability for new homeowners, according to Milliman.

Quantifying the Financial Impact

To drive policy change, NRDC needed hard data quantifying the financial risks to homebuyers. They partnered with Milliman, where Larry Baeder, a senior data scientist, co-authored a study titled, “Estimating undisclosed flood risk in real estate transactions.”

Using catastrophe models, proprietary datasets, real estate transaction data, historical flood events and demographic patterns, Baeder analyzed the impact in three states with low marks on NRDC’s Flood Risk Disclosure Laws Scorecard: North Carolina, New York and New Jersey.

The findings revealed staggering financial disparities. In North Carolina, a home without flood history might face an average annual loss (AAL) of about $60. In contrast, a flood-prone property’s AAL jumped to approximately $1,200 — 20 times higher — and could exceed $2,000 based on future flood projections. Over 15 years, previously flooded North Carolina properties might require more than $18,000 in repairs.

The numbers were even more concerning in the Northeast. In New York, flood history could increase a property’s AAL from about $100 to $3,000. A previously flooded New Jersey home might incur $25,000 in damages over a 15-year period.

“These are big numbers, and they’re a scary reality that people are going to have to deal with,” Baeder noted. “If a homebuyer is taking on this risk, they should be aware of the risk.” Milliman’s research also found that more than 6% of all homes sold across these three states in 2021 had a record of flooding—with no requirement to warn new owners about this history.

Data-Driven Legislative Change

Armed with Milliman’s analysis, NRDC approached lawmakers with compelling evidence of the problem’s scale and impact.

“Before the report, I think legislators knew that people struggled to rebuild after a flood,” Scata said, “but I don’t think they realized just how much it costs a homeowner. These numbers helped lawmakers see this was a big problem, that their constituents were suffering, and that they should do something about it.”

The data-driven approach proved effective. In 2023, New Jersey began legally requiring sellers to disclose a property’s flood history. North Carolina and New York soon followed, with New York enacting disclosure requirements at the end of 2023 and North Carolina amending mandatory forms in 2024.

The impact extended beyond these three states. Four additional states — Florida, Maine, New Hampshire and Vermont — independently adopted disclosure requirements in 2024 after recognizing the need demonstrated elsewhere.

“The laws show the power of data,” Scata noted. “Having Milliman do this work was really important for showing the actual impacts of flood damage on homeowners and effecting change through the legislatures.”

The momentum continues as Baeder now leads a follow-up study for NRDC expanding the research to 25 additional states with insufficient disclosure laws. Scata hopes to eventually see strong disclosure requirements nationwide, providing all homebuyers and renters with insight into their flood risk.

“If we’re going to tell people about lead-based paint,” Scata concludes, referring to other widespread real estate disclosures, “if we’re going to tell people about asbestos, we should probably tell people about flooding, because flooding has such an impact on someone’s finances and health.”

The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

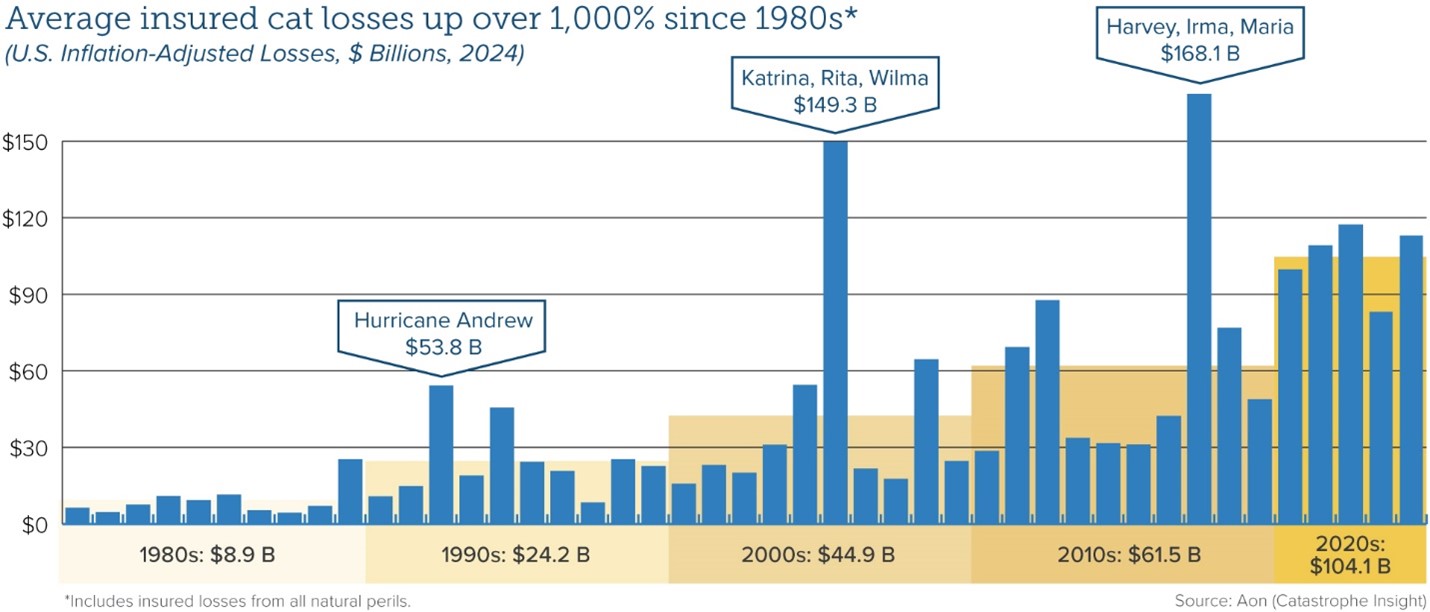

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

Chief Economist and Data Scientist, Dr. Michel Léonard

Recent tariffs issued by U.S. President Donald Trump are on track to increase the price of parts and materials used in repairing and restoring property after an insurable event. Analysts and economists, predict these price hikes will lead to higher claim payouts for P&C insurers and, ultimately, higher premiums for policyholders.

After making several announcements since early March 2025, on April 2, President Trump signed an executive order imposing a minimum 10 percent tariff on all U.S. imports, with higher levies on imports from 57 specific trading partners. A general tariff rate became effective on April 5, while tariffs on imports from the targeted nations, ranging from 11 to 50 percent, took effect on April 9. A 25 percent tariff applies to all steel and aluminum imports and cars. President Trump says he might consider a one-month exemption to the auto industry, but as of this writing, no changes have been issued.

Generally, tariffs can bring in revenue for the issuing government but lower the operating margin for impacted domestic businesses. Inventory and supply chain managers may attempt to stockpile in advance of the new rates becoming effective, which in turn can spike demand and quickly spike prices for sought-after items. Eventually, these cost hikes get passed on to consumers.

Nonetheless, to ride out the situation, inventory and supply chain managers need a fundamental level of predictability regarding what the levies will cover, what the rates are, and when these rates go into effect. The timing and scope of President Trump’s tariff policies have been challenging to nail down, including for many goods particularly relevant to construction and auto manufacturing. For example, his initially declared rates for major trading partners – Canada, Mexico, the European Union, and China – have fluctuated as these nations announced reciprocal tariffs, and those levies, in turn, were met with higher US rates.

Then, on April 9, President Trump declared a 90-day pause on tariffs. This change was actually not a true pause but a reduction of previous rates for several countries to 10 percent, except for China. The White House has declared on April 10 that the previously announced 125 percent rate against goods from China is actually now 145 percent.

According to S&P, the levy on auto industry imports has been comparatively less dynamic as, despite confusing announcements from the White House, there has been no change to President Trump’s 25 percent rate declared on March 26, “which applies to all light-vehicle imports, regardless of country. The 25 percent tariff includes auto parts as well as completely built up (CBU) vehicles. The CBU autos tariff went into effect on April 3, 2025, while the auto parts portion is due to come into effect on May 3, 2025.”

As insurers grapple with risk management and inflationary pressures, other challenges posed by the tariffs can include issues for policyholders, specifically coverage affordability and availability. One downstream side effect may be the increased risk of expanding the protection gap – uninsurance and underinsurance (UM/UIM) due to higher premiums and higher valuations that can come into play when materials costs rise. Across the fifty states and the District of Columbia, one in three drivers (33.4 percent) were either uninsured or underinsured in 2023, according to a recent report, Uninsured and Underinsured Motorists: 2017–2023, by the Insurance Research Council (IRC), affiliated with The Institutes.

Our Chief Economist and Data Scientist, Dr.Michel Léonard, shares his analysis of how the tariffs may impact the P&C Insurance industry.

“There’s no crystal ball”, say Dr. Léonard, “but prudent risk underwriting and risk management suggests the use of scenarios and increased price ranges for different tariff levels, the more precise impact of which can be updated based on actual price increases for individual prices.”

Dr. Léonard outlines three types of P&C replacement cost scenarios given different tariff ranges:

1) For single-digit tariffs, while inventories last, higher prices below that tariff’s rate;

2) for single-digit tariffs on goods still economically viable post-tariffs, higher prices up to the tariff’s rate; and

3) for single and double-digit tariffs on goods no longer economically viable, a multiple of the pre-tariff price for tariff-evading goods.

Triple-I remains committed to keeping abreast of these and other developments crucial to the insurance industry’s future. For more information, we invite you to stay tuned to our blog and join us at JIF 2025.

A record number of bills targeting third-party litigation funding are under consideration across the United States, with Georgia and Kansas already passing disclosure measures, according to an analysis by Insurance Insider.

The U.S. Government Accountability Office defines third-party litigation funding as “an arrangement in which a funder who is not a party to the lawsuit agrees to help fund it.” Global multi-billion-dollar investing firms have made it their sole or primary business and are experiencing strong growth. Because the market lacks transparency, estimates on its size can vary but, according to Swiss Re, more than half of the $17 billion invested into litigation funding globally in 2020 was deployed in the United States. Swiss Re estimates the market will be as high as $30 billion by 2028.

Meanwhile, affordability of insurance coverage – especially for commercial auto products – has come under threat from increases in litigation and claim costs. The national surge in legislation seeking to rein in this practice reflects growing concerns about its lack of transparency and undue influence of litigation financing by dark-money investors – many of them outside the United States.

Thirty-five separate bills have been introduced in U.S. statehouses so far this year. The Kansas bill was signed into law by Gov. Laura Kelly, and the Georgia bill is expected to be signed by Gov. Brian Kemp. Similar legislation is advancing through various committees in Arizona, California, Massachusetts, New Jersey, and Oklahoma and have been proposed in more than two dozen other states.

The efforts are not only progressing at the state level. The U.S. House of Representatives is advancing HR 1109 – The Litigation Transparency Act of 2025 – which would regulate third-party litigation funding in federal court cases. A similar bill was introduced in 2024 but did not advance out of committee.

Third-party litigation funding is just one aspect of the larger issue of legal system abuse that contributes to challenges related to property/casualty insurance availability and affordability.

Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that impede progress, according to the most recent Triple-I Issues Brief.

Like many states, California has suffered greatly from climate-related natural catastrophe losses. Like some disaster-prone states, it also has experienced a decline in insurers’ appetite for covering its property/casualty risks.

But much of California’s problem is driven by regulators’ application of Proposition 103 – a decades-old measure that constrains insurers’ ability to profitably write business in the state. As applied, Proposition 103 has:

Kept insurers from pricing catastrophe risk prospectively using models, requiring them to price based on historical data alone;

Barred insurers from incorporating reinsurance costs into pricing; and

Allowed consumer advocacy groups to intervene in the rate-approval process, making it hard for insurers to respond quickly to changing market conditions and driving up administration costs.

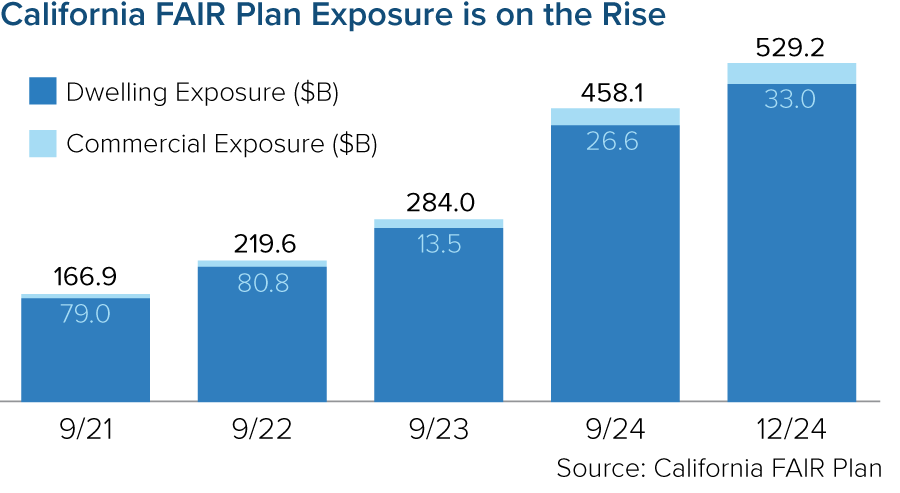

As insurers have adjusted their risk appetite to reflect these constraints, more property owners have been pushed into the California FAIR plan – the state’s property insurer of last resort. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for larger homeowners, condominium associations, homebuilders and other businesses.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to alleviate these pressures. The strategy has generated positive impacts, but it continues to meet resistance from legislators and consumer groups. And, regardless of what regulators or legislators do, California homeowners’ insurance premiums will need to rise.

The Triple-I brief points out that – despite the Golden State’s many challenges – its homeowners actually enjoy below-average home and auto insurance rates as a percentage of median income. Insurance availability ultimately depends on insurers being able to charge rates that adequately reflect the full impact of increasing climate risk in the state. In a disaster-prone state like California, these artificially low premium rates are not sustainable.

“Higher rates and reduced regulatory restrictions will allow more carriers to expand their underwriting appetite, relieving the availability crisis and reliance on the FAIR plan,” said Triple-I Chief Insurance Officer Dale Porfilio.

With events like January’s devastating fires, frequent “atmospheric rivers” that bring floods and mudslides, and the ever-present threat of earthquakes – alongside the many more mundane perils California shares with its 49 sister states – premium rates that adequately reflect the full impact of these risks are essential to continued availability of private insurance.

U.S. property claims volume rose 36 percent in 2024, propelled by a 113 percent increase in catastrophe claims, according to a recent Verisk Analytics report.

While evolving climate risks fueled claim frequency, uncertain inflation trends and unchecked legal system abuse will likely further strain insurer costs and time to settle these claims, posing risks to coverage affordability and availability.

Abnormally active Atlantic hurricane season

In a “dramatic shift” from previous loss patterns, late-season hurricane activity – rather than winter storms – dictated fourth-quarter claims operations last year, Verisk reported. Hurricane-related claims comprised nearly 9 percent of total claims volume, at a staggering 1,100 percent increase from the third quarter of 2023. Flood and wind claims both also jumped by 200 percent in volume.

“This shift in risk patterns demands new approaches to risk assessment and resource planning, particularly in the Southeast, where costs increased at six times the national rate following hurricane activity,” Verisk stated. Notably, Hurricane Milton generated roughly 187,000 claims totaling $2.68 billion in replacement costs across the Southeast, with 8 percent of claims still outstanding as of the report’s release.

Another above-average hurricane season is projected for 2025 in the Atlantic basin, according to a forecast by Colorado State University’s (CSU) Department of Atmospheric Science. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach, the CSU research team forecasts 17 named storms, including nine hurricanes – four of them “major” – during the 2025 season, which begins June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, three of them major. Major hurricanes are defined as those with wind speeds reaching Category 3, 4, or 5 on the Saffir-Simpson Hurricane Wind Scale.

Water, hail, and wind events in the Great Plains and Pacific Northwest also contributed to unexpected claim volumes, Verisk added. In contrast, wind-related claims fell in the Northeast compared to the fourth quarter of 2023.

Such regional variations highlight “the importance of granular, location-specific analysis for accurate risk assessment,” Verisk stated.

Contributing economic factors

Labor and material costs continued to rise year over year, with commercial reconstruction costs seeing a more pronounced increase of 5.5 percent compared to residential’s 4.5 percent, Verisk reported. The firm projected moderate reconstruction cost increases within both sectors during the first half of 2025.

Looming U.S. tariffs, however, may complicate this trajectory. Inflationary pressures related to the Trump Administration’s tariffs could further disrupt supply chains still recovering from natural catastrophes and the COVID-19 pandemic. Any such disruptions would compound replacement costs for U.S. auto and homeowners insurers as material costs – such as lumber, a major import from Canada – become even more expensive.

Excessive litigation trends

Similarly, excessive claims litigation – which prolongs claims disputes while driving up claim costs – plagues several of the states Verisk identified as experiencing increased claim volumes. For instance, though hurricane activity helps explain higher claim frequency in Georgia, the Peach State also is home to a personal auto claim litigation rate more than twice that of the median state, with a relative bodily injury claim frequency 60 percent higher than the U.S. average.

Verisk’s preliminary Q4 data reveals a 7 percent decrease in average claims severity compared to the same period in 2023 – a figure the firm expects to rise as more complex claims reach completion. But costly and protracted claims litigation, paired with ongoing tariff uncertainty, could magnify this figure even beyond their projections.

Undoubtedly, both will challenge insurers’ capacity to reliably predict loss trends and set fair and accurate premium rates for the foreseeable future, underscoring Verisk’s point that “staying ahead of these evolving patterns is essential in building more resilient operations in the future.”