MEMBERSHIP

AMPLIFY

EN ESPAÑOL

Connect With Us

- Popular search terms

- Automobile

- Home + Renters

- Claims

- Fraud

- Hurricane

- Popular Topics

- Automobile

- Home + Renters

- The Basics

- Disaster + Preparation

- Life Insurance

Triple-I defines Legal System Abuse as policyholder or plaintiff attorney practices which increase costs and time to settle insurance claims. While litigation is considered a policyholder’s last resort, legal system abuse exploits litigation when a disputed claim could have been resolved without judicial intervention. Legal system abuse contributes to higher costs for insurance operations and policyholder pricing.

Four big issues contribute to legal system abuse in the U.S., the biggest cost driver of social inflation, the Insurance Information Institute has found. Legal system abuse refers to disputed insurance claims which could have been resolved without litigation.

The consequences of legal system abuse, and the social inflation it causes, are significant. Higher costs for the insurance ecosystem increase the price of insurance coverage for all consumers and businesses.

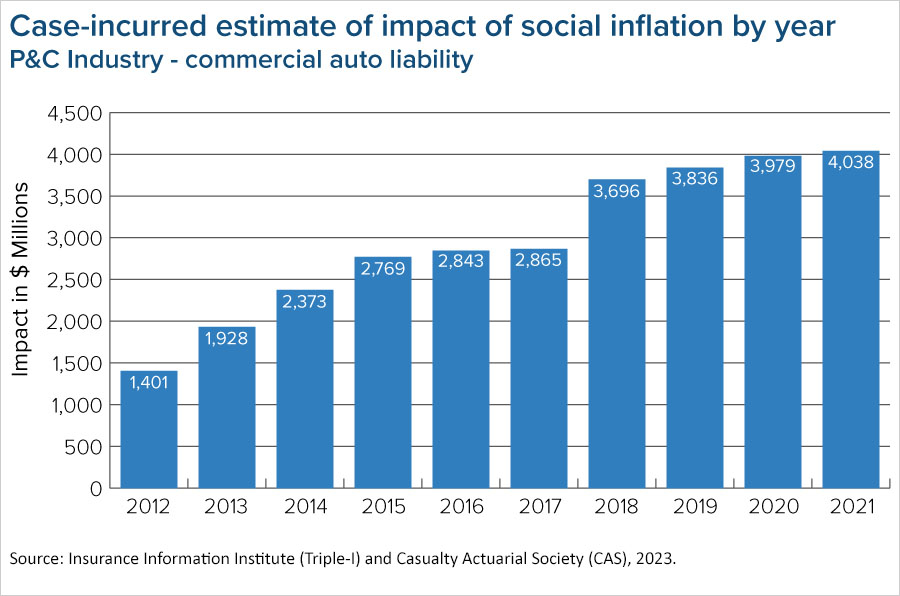

Social inflation drives higher insurer claim payouts and loss ratios. Ultimately, policyholders pay more for coverage. A simple way to think about social inflation and its components is to compare the impact of these factors on claims losses over time with growth in an inflation measure like the Consumer Price Index (CPI). The insurance lines that tend to bear the brunt are commercial auto, professional liability, product liability, and directors and officers liability. However, evidence indicates that pressure is mounting on private passenger automobile insurance, too.

By increasing claims costs, social inflation threatens the affordability of insurance coverage. We are committed to advancing a solutions-oriented conversation involving insurers, policyholders, and policymakers (legislators, courts, regulators, etc.).

While social inflation remains hard to predict and mitigate, it is crucial to understand the factors at play and the risks to all stakeholders. We'll continue developing research and curating thought leadership resources to raise awareness. Follow our content here and on the Triple-I Blog to stay abreast of this critical issue.